If you’re like millions of other Americans, you have some outstanding debt. Credit cards, lines of credit, auto loans, and other forms of debt are common in most households and can either work for or against you when it comes time to build a new home.

Lenders consider several factors pertaining to your use of credit when reviewing your application for a mortgage, so even though you have outstanding debt, you may still be able to qualify for a mortgage.

Here are a few of the factors that could have an effect on your ability to build a new home.

Debt-to-Income Ratio

An important factor in determining your qualification for a mortgage is your debt-to-income ratio(DTI). Essentially, this is how much debt you carry against how much income you have in your household. Most forms of income can be included, such as primary and secondary employment, child support payments, and alimony.

The debts considered include secured and unsecured loans, outgoing child support or alimony payments, as well as your current rent or mortgage payments. Not included are items such as groceries, utilities, and taxes.

To calculate your debt-to-income ratio, simply add up your total monthly debt payments and divide by your total monthly income. There are also a number of online calculators that can do this for you.

Most lenders will approve applicants whose debt-to-income ratio is less than 35%. If it’s between 36% to 49%, you may be conditionally approved with some debt required to be paid down first.

Typically, any ratio higher than 50% will be required to reduce your overall debt before being able to qualify for a mortgage.

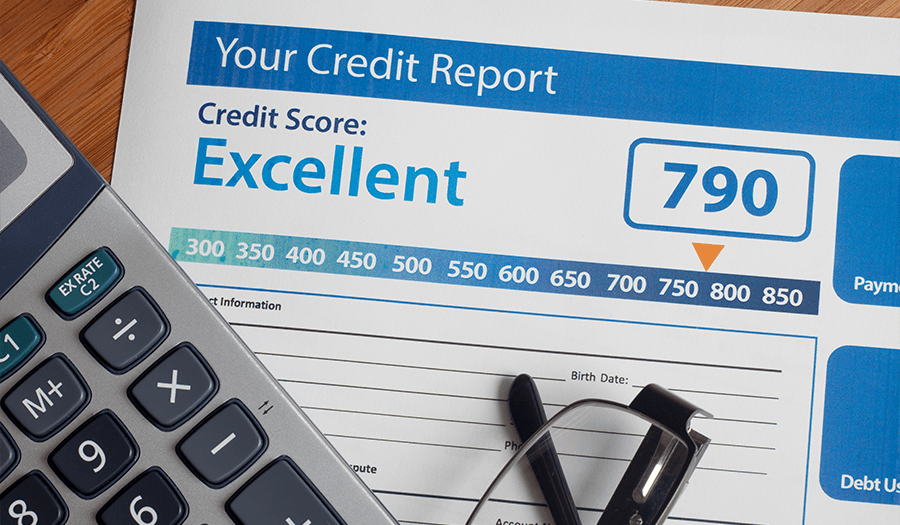

Credit Score

Your credit score is a number between 300 and 900 that indicates how responsibly you use credit. Anything over 650 is ideal, but the higher your score, the more likely you are to be approved and offered more competitive interest rates.

Your credit score is usually updated every two weeks, depending on how often your creditors report your activity. It can fluctuate based on your current credit use.

It’s a common misconception that having zero debt on your credit bureau will result in a good credit score, but the opposite is true. You need some credit activity to show your level of responsibility and positively affect your score.

Keep your credit cards paid off each month but utilize at least 20% of your open balance if you can. Pay your auto loan payments and existing mortgage payments on time, and don’t miss any. Pay down or pay off any high-interest credit cards or loans to reduce your outgoing payments.

If you find you struggle to pay down a balance due to high interest, contact your creditor to negotiate a lower interest rate. Many lenders are open to these discussions and will be happy to offer you options that will help you reduce your debt load.

To find out your credit score, you can order a report online.

Cash On Hand

In order to start building a new home, you’ll need a certain amount of cash on hand as part of the process. A down payment is required, which can be anywhere from 3.5% to 20% of the loan amount.

You’ll also need to cover the closing costs to take possession of your new home, including legal fees, title transfer, property tax, and other such fees.

Depending on the lender you’re applying to, they may require an additional reserve of funds set aside for mortgage principal, taxes, interest, and insurance payments.

Construction Loan Requirements

If you’re applying for a construction loan – a temporary loan that finances the construction phase of your new home – you may be required to provide some additional information. You’ll need to verify your income and review your latest tax return and pay stub. For those applicants who are self-employed, two years of tax returns will be required.

How a construction loan works is that the builder receives milestone payments directly from your lender throughout the build. Once your new home’s construction is complete, the lender typically converts your construction loan into a traditional mortgage.

While you may have some outstanding debt, it is still very possible to qualify for a mortgage and build a new home. Doing your due diligence to determine your credit score, your debt-to-income ratio, and assess your overall financial situation will help you decide if you need to pay off or pay down some debt before applying for a mortgage.

If in doubt, speak to a custom home builder. They often have skilled staff who can help guide you through the financial process of mortgage qualification.